This article is part of our series on the state of stablecoins as a foundation.

Stablecoins are digital dollars designed to maintain a stable value, usually pegged—or tracked— to the value of assets such as the USD, Euro, or even government treasuries. Unlike Bitcoin and other cryptocurrencies known for price volatility, stablecoins are meant to provide a stable value, making them useful for payments and transfers. Since their introduction in 2014, stablecoins have become a key tool for online transactions, offering low-cost, fast, and stable value transfers. They combine the efficiency of digital payments with the reliability businesses and institutions need, making them useful for everything from cross-border payments to settling transactions without the need of a trusted intermediary.

Types of Stablecoins

Stablecoins come in different forms, each with its own method for maintaining a stable value and a different underlying asset or mechanism backing it. Here’s a breakdown:

Fiat-Backed Stablecoins

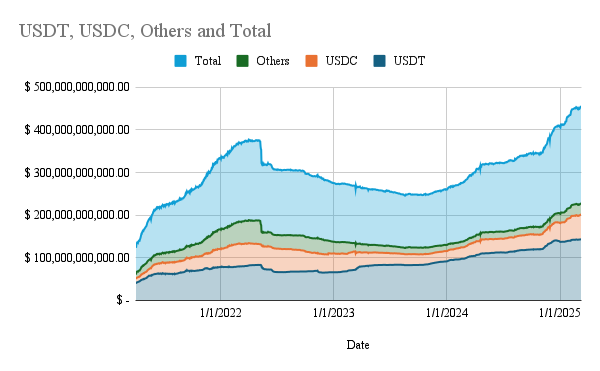

Fiat-backed stablecoins are the most widely used type of stablecoins, pegged to traditional currencies like the U.S. dollar or Euro and backed by cash and/or cash-equivalent reserves. Examples include USDT and USDC, which together account for over 90% of the $227 billion stablecoin market as of March 11th, 2025.

Their appeal lies in their simplicity—each coin is designed to be redeemable for one U.S. dollar, making them a practical tool for businesses looking to transfer funds across borders quickly and at a fraction of the cost of traditional methods.

Source: Defillama

Data as of 3/19/2025

However, not all fiat-backed stablecoins are equally transparent. While USDC is known for its regular public attestations and strict regulatory compliance, USDT has faced scrutiny due to the lack of a fully public reserve audit. Tether, the issuer of USDT, has never undergone a full public reserve audit, leading to ongoing concerns about the exact composition of its backing. This uncertainty has made some businesses and institutions cautious about integrating USDT into their financial operations, preferring more transparently managed alternatives

Tokenized Asset-Backed Stablecoins

These stablecoins are backed by tangible assets such as gold, commodities, or financial instruments like U.S. Treasuries. Gold-backed stablecoins, for example, represent a small but growing market—around $1.3 billion in early 2025 compared to $208 billion for fiat-pegged stablecoins. They can be useful in specific industries, such as mining or commodities trading, where settling transactions in asset-backed tokens can reduce currency conversion costs.

Treasury-backed stablecoins are becoming more integrated with traditional finance, offering a digital way to hold reserves in highly liquid, regulated assets. BlackRock’s BUIDL and Ondo Finance’s OUSG are prime examples, representing tokenized shares of short-term U.S. Treasuries and money market funds. These stablecoins combine the stability of traditional assets with the efficiency of digital transactions, providing an alternative to cash management tools while leveraging blockchain programmability to enable real-time disbursement of yield. By eliminating intermediaries and automating processes through smart contracts, they reduce the costs and delays associated with traditional financial infrastructure.

Crypto-Backed Stablecoins

These stablecoins are backed by other cryptocurrencies, meaning digital assets are locked up as collateral to issue stablecoins. Examples include Aave’s protocol stablecoin GHO and USDe from Ethena. They are primarily used within crypto markets for onchain trading, lending, and Decentralized Finance (DeFi) applications, allowing users to move value across blockchain networks without needing to convert back to traditional currency. However, since these stablecoins use volatile assets as collateral, they must be over-collateralized - meaning the value locked up often exceeds the amount of stablecoins issued - to maintain a 1:1 peg and absorb potential depegs. While mechanisms like liquidation and various fees help them keep their pegs, crypto-backed stablecoins' dependence on the crypto market conditions makes them less practical for business use cases like payroll or supplier payments, where price stability and predictable liquidity are essential. As of early 2025, all crypto-backed stablecoins combined have a market cap of approximately $19 billion, a small but significant share of the broader stablecoin market.

Algorithmic Stablecoins

These stablecoins use automated mechanisms to manage supply and demand in an effort to maintain a stable value—without being backed by physical assets. While an interesting concept, they have proven risky. The collapse of Terra’s algorithmic stablecoin UST in 2022 resulted in over $60 billion in losses and damaged trust in this approach. Frax (FRAX) is one of the few algorithmic stablecoins that has persisted, though it has experienced periods of depegging. It has since transitioned to being partially backed by real-world assets in an effort to improve stability. Despite these efforts, algorithmic stablecoins remain a niche category, with a total market cap of just over $500 million as of March 11th 2025, a fraction of the broader stablecoin market. For businesses, reliability is key, making this type of stablecoin a risky choice.

How Businesses are Using Stablecoins

Stablecoins are increasingly used by corporations and financial institutions to streamline payments, reduce costs, and improve settlement efficiency. For example, Visa launched a USDC settlement pilot with Crypto.com in 2020 on Ethereum. Now, in 2025, the pilot has expanded to select merchants, allowing them to settle cross-border payments in minutes, bypassing intermediaries and reducing transaction costs. This is not about replacing cash but about improving payment infrastructure, and Visa’s expansion in this space signals growing institutional interest.

Other payment firms, including Stripe and Revolut, have integrated stablecoins to reduce fees and enhance transaction speed. Stripe began supporting USDC payouts in 2023 and strengthened this initiative with its $1.1 billion acquisition of Bridge in 2024, enabling businesses to accept digital dollars on blockchains like Solana and settle in fiat with lower costs. Revolut, meanwhile, uses USDC and USDT to help businesses pay international suppliers without incurring traditional foreign exchange fees of 1-3%, translating to savings of $10,000–$30,000 on a $1 million transaction.

Remittance providers are also adopting stablecoins to cut costs. MoneyGram launched a partnership with Stellar in 2022 to enable USDC-based transfers, allowing users to send and receive funds with lower fees and faster settlement times compared to traditional remittance services. Since then the service has expanded past the initial test markets to Southeast Asia, Africa, and Latin America—regions where remittance fees remain prohibitively high. In these areas, stablecoin remittances provide an alternative for individuals and businesses that rely on international payments but face high banking costs, slow processing times, and limited financial access.

While these use cases highlight stablecoins' practical applications, their overall transaction volume is still dominated by crypto trading activity. In 2024, total stablecoin transfer volume reached $27.6 trillion, surpassing the combined transaction volume of Visa and Mastercard by 7.68%. However, a large portion of this volume came from trading activity on centralized exchanges (CEXs) and decentralized exchanges (DEXs), where stablecoins serve as the primary trading pair. Despite this, stablecoins’ increasing adoption in real-world payments suggests they are becoming more than just a tool for crypto markets, with financial institutions leveraging them for settlement efficiency and cost savings.

Market Size and Major Players

The stablecoin market is diverse, with established leaders, new entrants, and innovative models like white-label stablecoins offering tailored solutions for businesses.

Market Size

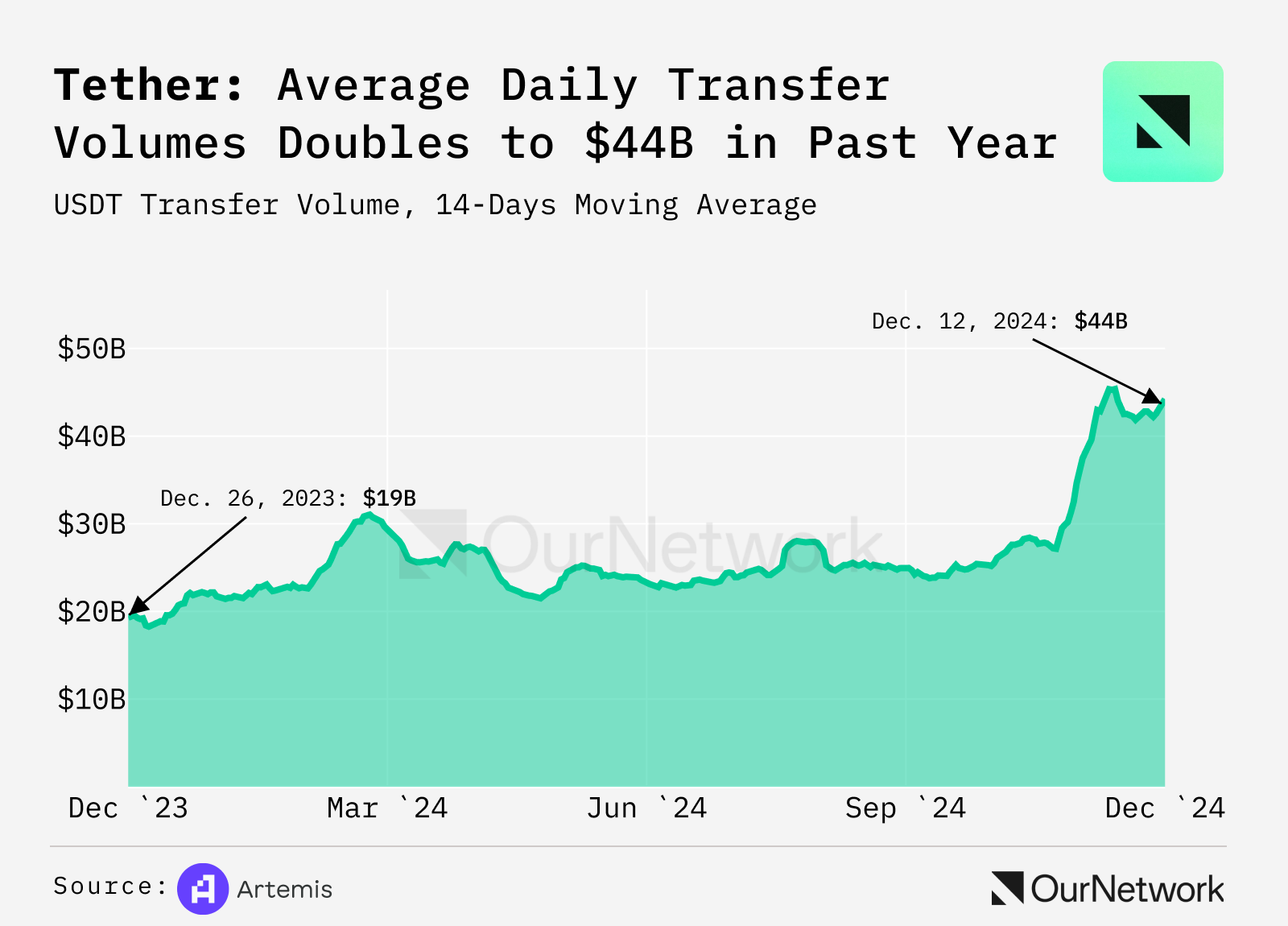

As of March 11th 2025, the stablecoin market exceeds $227 billion in circulating supply, with USDT’s daily transaction volumes alone often surpassing $20 billion. This scale rivals some traditional payment networks, making stablecoins a credible alternative for payments.

Source: OurNetwork, Artemis

Data as of 12/31/24

Major Players

Tether and Circle, the two largest stablecoin issuers, collectively hold over $204 billion in U.S. Treasuries—making them the 14th largest holder globally. Their combined treasury holdings surpass those of entire nations, including Norway and Brazil.

Tether (USDT): The largest stablecoin by market cap, with roughly $142 billion in circulation, Tether dominates due to its liquidity and widespread acceptance. However, its opaque reserve practices raise concerns for risk-averse corporations. Tether is the most profitable company in the world per employee, largely due to its ability to capture the yield generated from the U.S. treasuries that back its stablecoin.

Tether’s business model is straightforward but highly lucrative. When users purchase USDT, they deposit U.S. dollars with Tether, which the company then invests primarily in short-term U.S. treasuries. Because these assets are low-risk, highly liquid, and yield-bearing, Tether benefits from the interest income generated. With short-term treasury yields currently around 4-5%, Tether is able to passively earn billions in interest while incurring minimal operational costs. Unlike traditional banks, which pay depositors interest on their holdings, Tether retains the full yield from these treasuries, making it a cash machine - this is a strategy that all non-yield-bearing stablecoin providers employ.

USD Coin (USDC): Backed by Circle, BlackRock, and Coinbase, USDC has amassed a market cap of over $56 billion. Its transparency and U.S. regulatory compliance make it a safer bet for enterprises.

Emerging Models: White-Label Stablecons and Their Benefits

These types of stablecoins allow businesses to issue branded stablecoins backed by established providers (e.g., Bastion). For instance, ACME Corp could launch “ACME Coin” for supplier payments, pegged 1:1 to the dollar, without having to build blockchain infrastructure from scratch. This model offers several key advantages:

- Cheaper Global Transactions & Ecosystem Control – By issuing their own stablecoin, businesses can significantly reduce transaction fees, particularly for international payments, while maintaining control over their financial ecosystem. Transactions within their network are streamlined, ensuring value retention and minimizing reliance on third-party payment processors.

- New Revenue Streams & Monetization Opportunities – Companies can monetize on-ramps and off-ramps by charging fees for converting between fiat currency and their stablecoin. Additionally, by facilitating cross-border transactions, they can generate transaction fees through global partnerships.

- Interest on Reserves & Capital Efficiency – A branded stablecoin enables businesses to earn yield on the reserves backing their digital currency. These reserves, typically held in government securities or interest-bearing accounts, can generate revenue that subsidizes rewards programs, enhances operational efficiency, and turns passive assets into active revenue streams.

- Enhanced Customer Engagement & Loyalty – Stablecoins can drive user and merchant acquisition by creating a seamless, branded transaction experience. Companies can offer loyalty programs, cashback rewards, and incentives funded by the interest earned on stablecoin reserves. For example, Target could provide customers with discounts or additional perks when using “Target Coin” for purchases, strengthening brand affinity.

- Data-Driven Insights & Extended Reach – With a proprietary stablecoin, businesses gain visibility into transaction patterns across their extended network. These insights can drive strategic decisions, optimize merchant relationships, and enhance customer targeting efforts. Additionally, the ability to facilitate transactions both within and outside their ecosystem helps businesses expand their reach and market influence.

By leveraging branded stablecoins, businesses not only improve financial efficiency but also unlock new monetization avenues while enhancing customer loyalty and market presence. This approach positions companies at the forefront of the evolving digital payments landscape, aligning with the broader shift toward blockchain-based financial infrastructure.